by LLT | Mar 24, 2017 | LLT, News

How more granular information will change lending behavior

How more granular information will change lending behavior

With foreclosures at a 10-year low, a good case can be made to take a look at strict lending standards that may be doing more harm than good.

For example, during the period immediately following the housing bust, from 2009 to 2014, 5.2 million mortgages that would have passed muster under cautious lending standards in place for many years before they slackened during the housing boom were denied.

Today’s standards, except for FHA borrowers, haven’t changed much since then.

Some proponents believe new techniques to analyze creditworthiness, like trended data, will also help some marginal borrowers qualify for loans.

Trended credit data takes a deeper dive into creditworthiness than the snapshots provided by credit scores and looks at multiple snapshots going backward in time to track trends in past behavior.

Trended data reports include up to 24 months of tradeline level credit information such as balance, credit limit, high credit, scheduled payment and actual payment. It exposes much more granular data about a borrower’s payment history on a monthly basis than traditional credit histories.

Will trended credit result in more approvals?

Late last year, Fannie Mae required trended data for its automated underwriting software, Desktop Underwriter.

“Leveraging trended data in the DU risk assessment allows a smarter, more thorough analysis of the borrower’s credit history. The use of trended data is a powerful predictor of risk, and its use enhances the DU risk assessment to better support access to credit for creditworthy borrowers,” said Fannie in its release notes to lenders.

An Equifax December 2016 Consumer Credit Impact analysis found that on an annual basis the addition of trended credit data could result in 4 percent, or 267,000, more mortgages or improved loan terms for consumers who may have previously been ineligible.

Also, 4.1 percent or 65,000 more home equity lines of credit (HELOC) were issued to consumers who may have previously been ineligible.

In fact, in its notes to underwriters accompanying the new release of Desktop Underwriter, Fannie Mae said trended credit is expected to have minimal to no impact on the percentage of Approve/Eligible recommendations that lenders receive today.

Continue reading.

![Mortgage rates fall back as investors’ concerns mount]()

by LLT | Mar 23, 2017 | LLT, News

Mortgage rates retreated this week after a one-week spike following the Federal Reserve’s decision to raise its benchmark rate.

According to the latest data released Thursday by Freddie Mac, the 30-year fixed-rate average fell to 4.23 percent with an average 0.5 point. (Points are fees paid to a lender equal to 1 percent of the loan amount.) It was 4.30 percent a week ago and 3.71 percent a year ago.

According to the latest data released Thursday by Freddie Mac, the 30-year fixed-rate average fell to 4.23 percent with an average 0.5 point. (Points are fees paid to a lender equal to 1 percent of the loan amount.) It was 4.30 percent a week ago and 3.71 percent a year ago.

The 15-year fixed-rate average dropped to 3.44 percent with an average 0.5 point. It was 3.50 percent a week ago and 2.96 percent a year ago. The five-year adjustable rate average slid to 3.24 percent with an average 0.4 point. It was 3.28 percent a week ago and 2.89 percent a year ago.

“This marks the greatest week-over-week decline for the 30-year mortgage rate in over two months, a stark contrast from last week’s jump following the FOMC announcement,” Sean Becketti, Freddie Mac chief economist, said in a statement.

Financial markets had been betting on fiscal stimulus through tax cuts and infrastructure spending. Instead, President Trump has been bogged down by the health care overhaul bill. Anxious investors worry that health care reform will tie up Congress and delay implementation of Trump’s other policies.

Because of these concerns, they have been moving from stocks to bonds, driving down yields. The yield on the 10-year Treasury has plummeted 22 basis points — a basis point is 0.01 percentage point — since March 13.

Mortgage rates tend to follow the movement of long-term bonds. When the yield on the 10-year Treasury falls typically so do home loan rates.

Experts are divided on where rates are headed. Bankrate.com, which puts out a weekly mortgage rate trend index, found that more than half the experts it surveyed said rates will remain relatively stable in the coming week, moving less than two basis points up or down. About a third of the experts said rates will fall. Greg McBride, chief financial analyst at Bankrate.com, was among them.

Continue reading.

by LLT | Mar 22, 2017 | LLT, News

Fourth quarter produces highest quality loans since 2001

Fourth quarter produces highest quality loans since 2001

Mortgage originations grew safer in the fourth quarter of 2016, according to CoreLogic, a global property information, analytics and data-enabled solutions provider.

Mortgage became less risky in from the year before, according to the Q4 2016 CoreLogic Housing Credit Index. This is consistent with the low credit risk from the third quarter and the highest quality home loans originated since 2001.

The index measures variations in home mortgage credit risk attributes over time, including borrower credit score, debt-to-income ratio and loan-to-value ratio. A rising HCI indicates that new single-family loans have more credit risk than during the prior period, while a declining HCI means that new originations have less credit risk.

“Mortgage loans closed during the final three months of 2016 had characteristics that contribute to relatively low levels of default risk,” CoreLogic Chief Economist Frank Nothaft said.

“While our index indicates somewhat less risk than both a quarter and a year earlier, this partly reflects the large refinance share of fourth-quarter originations,” Nothaft said. “Refinance borrowers typically have a lower LTV and DTI than purchase borrowers.”

But this influx in refinances may have much less of an effect on the next quarter’s index as interest rates rise.

“Refinance volume will decline with higher mortgage rates, and lenders generally will respond by applying the flexibility in underwriting guidelines to make loans to harder-to-qualify borrowers,” Nothaft said.

“As this occurs, we should observe our index signaling a gradual increase in default risk,” he said. “The evolution to a more purchase-dominated lending mix is also likely to increase fraud risk.”

During the quarter, the average credit score for homebuyers increased four points annually to 737. The share of homebuyers with credit scores under 640 hit one-tenth of those in 2001. The DTI average remained at 36% during the fourth quarter. And LTV for homebuyers increased less than 1% from last year to 87.1%.

Read the full article.

by LLT | Mar 21, 2017 | LLT, News

Closing times were way down in February, falling from 51 days in January to 46 days for all loans last month, according to the latest Ellie Mae Origination Insight Report.

Closing times were way down in February, falling from 51 days in January to 46 days for all loans last month, according to the latest Ellie Mae Origination Insight Report.

Broken out, home purchase loans took an average of 45 days to close in February, down from 48 days in January. Refinanced loans took an average of 47 days to close in February, down from 53 days.

Conventional loans commanded 63 percent of the market share, compared to 66 percent in January, according to Ellie Mae’s report. The FHA increased its market share by 2 percentage points to 23 percent, and VA loans rose by 1 percentage point to 10 percent.

FICO scores on closed loans decreased moderately in February, dropping from 722 in January to 720 in February. Ellie Mae’s report shows that average FICO scores are 11 points lower than the highs reached a year ago in August and September. Still, FICO scores are one point higher than the beginning of 2016.

Seventy percent of all closed purchase loans had scores of 700 or more.

“The purchase market led the way in February, representing 57 percent of total closed loans,” says Jonathan Corr, president and CEO of Ellie Mae. “Along with the growing purchase market, we’re seeing the time to close all loans decrease and FICO scores decline, trends that we will continue to watch in the coming months.”

Read the full article.

by LLT | Mar 20, 2017 | LLT, News

The winning bidder of a Grand Rapids, Michigan, house has been offered almost $20,000 to hand his purchase contract to another buyer. An agent in Nashville, Tennessee, got a property for his client by cold-calling local homeowners. Near Columbus, Ohio, it took a teacher five tries to secure a deal.

The winning bidder of a Grand Rapids, Michigan, house has been offered almost $20,000 to hand his purchase contract to another buyer. An agent in Nashville, Tennessee, got a property for his client by cold-calling local homeowners. Near Columbus, Ohio, it took a teacher five tries to secure a deal.

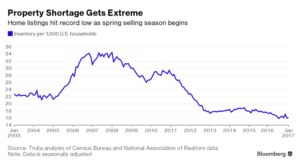

It’s the 2017 U.S. spring home-selling season, and listings are scarcer than they’ve ever been. Bidding wars common in perennially hot markets like the San Francisco Bay area, Denver and Boston are now also prevalent in the once slow-and-steady heartland, sending prices higher and sparking desperation among buyers across the country.

“Homebuyers are going to find this spring that, in a lot of markets, the inventory of homes priced and sized at price levels they were hoping for will be very limited,” said Thomas Lawler, a former Fannie Mae economist who’s now a housing consultant in Leesburg, Virginia. “Unlikely places are getting significantly tighter.”

Buyers are clamoring as an improved job market and growing confidence in the economy collide with rising mortgage rates — yet there’s little new inventory for them to purchase. Housing starts remain well below levels before the last recession, and builders have focused on higher-end properties out of reach for many people. Homeowners have become even more reluctant to sell because, after all, where are they going to move?

The three months through January had the fewest homes on the market on record, according to an analysis by Trulia. Prices jumped 6.9 percent in January from a year earlier, the biggest increase for any month since May 2014, data from CoreLogic Inc. show. And homes sold faster in the first two months of 2017 — spending an average 58 days on the market — than at the start of any year since at least 2010, according to brokerage Redfin.

Homes are moving fastest in Denver, Seattle and Oakland, California — areas where heated competition have become status quo in recent years because of soaring job growth, particularly in the technology industry. But fourth on Redfin’s list is Grand Rapids, Michigan’s second-largest city, in a reflection of strengthening employment across even the slower-growing center of the country. Buyers are also struggling in cities such as Boise, Idaho; Madison, Wisconsin; and Omaha, Nebraska.

Continue reading.

Recent Comments