by LLT | Feb 27, 2017 | LLT, News

New Homes Continue To Sell Quickly

New Homes Continue To Sell Quickly

According to the U.S. Census Bureau, more than half-million new homes were sold on a seasonally-adjusted, annualized basis, continuing last year’s momentum.

But new home supply is higher than it’s been more than a year, and negotiating buyers could gain the upper hand versus builders in 2017.

For now, a favorable mortgage environment is pushing new home sales ahead.

Today’s mortgage rates are low, and lenders are loosening credit standards rapidly. The result: more mortgage applicants are getting approved.

And, coming up with a down payment is rarely a problem anymore.

A program requiring just 3.5% down is the popular FHA loan. Not to be outdone, the USDA mortgage, also known as the Rural Development Loan, requires absolutely nothing down.

Both programs can be used to buy a newly-constructed home.

New construction still provides great value, and it’s an excellent time to be new-home shopping.

New Home Sales Hit 555,000 Sales, Annualized

Each month, the U.S. Census Bureau and the U.S. Department of Housing & Urban Development (HUD) jointly release the New Home Sales report.

The report seeks to gauge the health of the new construction market.

A “new home” is one which has not been previously occupied, otherwise known as new construction.

For January 2017, HUD reports 555,000 new homes sold on a seasonally-adjusted, annualized basis, which was a 3.7 percent increase from the month prior, and 5.5% higher than one year ago.

The 2017 new home market is off to a stellar start, and home builders are optimistic.

Earlier this month, the National Association of Homebuilders (NAHB) released its Housing Market Index (HMI), a monthly homebuilder confidence survey.

The most recent Housing Market Index shows homebuilder confidence near its highest point in a decade, with home builders projecting sales for the first half of 2017 near multi-year bests.

Demand for new homes has been strong, too, as evidenced by the high number of buyers requesting tours of model units.

The good news for buyers, though, is that new home inventory is actually increasing.

Continue reading.

by LLT | Feb 24, 2017 | LLT, News

Home value appreciation is ramping up in housing markets across the South, led by cities in Tennessee, Florida and Texas.

Home value appreciation is ramping up in housing markets across the South, led by cities in Tennessee, Florida and Texas.

Nationwide, home values are up 7.2% year over year to $195,300, Zillow reported Thursday in its January Home Value Index.

Nashville experienced the highest year-over-year home value growth of the nation’s largest metropolitan areas at 12.4%, followed by Portland, Ore., and Tampa, Fla., at 12.1% and 11.9%, respectively. Other cities that have seen home values rise by more than 10% over the past year include Dallas-Fort Worth, Orlando, Fla., and Seattle.

“We spend a lot of time focusing on the West Coast, but powerhouse markets exist throughout the country,” Zillow Chief Economist Svenja Gudell said in a news release.

“Florida and Texas home values have grown quite a bit over the past several years, stealing the spotlight from slower moving markets like San Francisco, San Jose and Los Angeles. Slowdowns in the Bay Area, in particular, are driven by the fact that these markets are so expensive that many people can no longer realistically afford to buy there, limiting demand and reducing pressure on home values.”

Looking ahead, Gudell predicted that home value growth will slow throughout the rest of 2017 as a result of rising mortgage rates and worsening affordability nationwide.

Read the full article.

by LLT | Feb 23, 2017 | LLT, News

Americans shrugged off rising mortgage rates and bought existing homes in January at the fastest pace since 2007. That has set off bidding wars that have pushed up prices as the supply of available homes has dwindled to record lows.

Americans shrugged off rising mortgage rates and bought existing homes in January at the fastest pace since 2007. That has set off bidding wars that have pushed up prices as the supply of available homes has dwindled to record lows.

Home sales rose 3.3% in January from December to a seasonally adjusted annual rate of 5.69 million, the National Assn. of Realtors said Wednesday.

Steady job gains, modest pay raises and rising consumer confidence are spurring healthy home buying even though borrowing costs have risen since last fall. Some potential buyers may be accelerating their home purchases to get ahead of any further increases in mortgage rates. With few homes available for sale, buyers feel pressure to rapidly close a deal when they find a suitable property.

The typical house for sale was on the market for just 50 days last month, down from 64 days a year earlier. Strong demand is pushing up the median home price, which jumped 7.1% from a year earlier to $228,900.

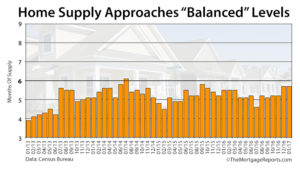

Just 1.69 million homes were on the market nationwide in January, near the lowest level since records began in 1999. It would take 3.6 months to deplete that supply at the current pace of sales, matching a record low reached in December. In a balanced housing market, supply is usually equal to about six months’ worth of sales.

The supply crunch probably will get worse during the upcoming spring buying season, economists say, because demand typically rises by more than supply during that time.

“Relative to the number of households, the number of homes for sale is well through prior historic lows,” said Ted Wieseman, an economist at Morgan Stanley. “The level of inventories could be a much bigger challenge moving into much higher sales in the spring and summer.”

That, combined with higher mortgage rates, soon could restrain sales.

Continue reading.

by LLT | Feb 22, 2017 | LLT, News

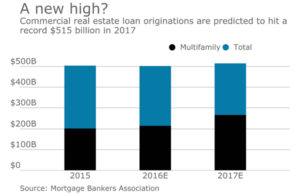

Commercial mortgage loan originations in 2017 are expected to increase 3% over last year to a record high, as market fundamentals and property prices remain strong, according to the Mortgage Bankers Association.

Commercial mortgage loan originations in 2017 are expected to increase 3% over last year to a record high, as market fundamentals and property prices remain strong, according to the Mortgage Bankers Association.

It projects total volume of $515 billion, with multifamily lending making up $267 billion. For 2016, the MBA estimated that there was $502 billion of commercial real estate loans originated, down from 2015’s $504 billion. Final numbers are expected to be released in March.

The current record year for CRE volume is $508 billion, set in 2007.

“Nationally, commercial real estate fundamentals and prices remain strong. That overall strength is expected to continue to support active sales and mortgage markets.

“Rising interest rates are likely to take a bit of wind out of the market, but even so, modest increases in originations should bring 2017 to record levels of borrowing and lending for commercial, and particularly multifamily, properties,” Jamie Woodwell, MBA’s vice president of commercial real estate research, said in a press release issued Monday.

By investor type, loans originated last year to support commercial mortgage-backed securities fell 15% compared with 2015, originations for life insurance companies were flat, commercial bank portfolio originations were up 6% and there was a 10% increase in loans originated for Fannie Mae and Freddie Mac.

Fannie Mae had $55.3 billion of multifamily loans originated through its Delegated Underwriting and Servicing program in 2016, which is the most that program has ever done, it said in a separate press release. It also issued $54.9 billion of CMBS in 2016.

Freddie Mac also set a record, with $56.8 billion of multifamily mortgages originated in 2016, it said in its own press release.

In the fourth quarter, there was a 7% year-over-year decline in CRE loan volume as there was a decrease in originations for hotel, health care and retail properties, the MBA said.

See the full article.

by LLT | Feb 21, 2017 | LLT, News

Mortgage payments make up the biggest chunk of U.S. homeowners’ income since 2010.

Mortgage payments make up the biggest chunk of U.S. homeowners’ income since 2010.

The average monthly mortgage payment made up 15.8% of buyers’ income in the fourth quarter of last year, according to real estate website Zillow, the biggest share of homeowner income since the second quarter of 2010, thanks to rising interest rates and increasing home values. The average monthly payment was $758 at the end of last year, up from $690 in 2015. Though it’s still not quite as bad as the national average of 21% between 1985 to 2000. “This is a phenomenon that really affects homebuyers a whole lot more,” said Svenja Gudell, chief economist at Zillow.

Affording a house will get a lot harder next year, and because banks have tightened restrictions on mortgage lending, some people aren’t even trying to apply for mortgages. People with low credit scores are especially at a disadvantage, as lenders have tougher expectations for borrowers to meet — the third quarter of 2016 saw the highest quality home loans since 2000, but that means those applying must have stellar credit scores (the average for loans originating in the third quarter of last year was 739).

But it could be worse, and in some cities, it is. Coastal cities see even higher shares of their income go toward their mortgages. In New York, for example, homeowners spent 27% of their income on their mortgage payments, and in San Francisco, it was more than 42%. There is one bright spot for those who have already bought homes: Current homeowners would obviously only be affected by rising interest rates if they chose an adjustable-rate mortgage, which fluctuates as opposed to a fixed-rate, Gudell said.

In general, the rule of thumb for buying a home is to spend no more than three times your income — so if you make $100,000, you should look for a house that costs about $300,000, Gudell said. It’s a rough estimate, and likely doesn’t apply to homes on the country’s coasts, in places like Los Angeles and New York.

Your monthly housing payment, including your principal, interest, taxes, insurance and in co-op and condo situations, home association fees, should not take up more than 28% of your salary before taxes, according to estimates by personal finance site Bankrate.com.

Continue reading.

by LLT | Feb 20, 2017 | LLT, News

Distressed Homes Drag Down The Neighborhood Home Prices

Distressed Homes Drag Down The Neighborhood Home Prices

Homeowners don’t like to see abandoned houses on their block. Zombie foreclosures—vacated homes that have yet to complete the foreclosure process—can be more than an eyesore. They may also attract crime and lower surrounding home prices.

If you’re shopping for a mortgage loan and a home, there’s good news on this front. Foreclosure rates are falling fast.

What New Data Reveal

Fresh numbers from ATTOM Data Solutions show that foreclosure activity nationally plunged to a 10-year low in 2016. Looking closer, U.S. foreclosure rates dropped by 30 percent last year.

That’s the most improvement of any year on record, according to Black Knight Financial Services. December 2016’s 59,700 foreclosure starts marked an amazing 24 percent decrease from the same period a year earlier.

Foreclosure filings surpassed 2.8 million in 2010. Last year, they tallied 933,045. That’s a sign that the housing market is in much better shape today than a few years ago.

Why Foreclosures Are Down

Daren Blomquist, senior vice president for ATTOM Data Solutions, says foreclosure filings are down for two reasons.

First, since the last housing bubble, there are fewer “legacy” foreclosures—meaning homes in the foreclosure process with loans originated between 2004 and 2008.

“Most legacy foreclosures have either been already foreclosed on or resolved in some other way, such as refinancing, modification or short sale,” says Blomquist.

Second, “loans originated over the past seven years are holding up well, with default rates below historically normal levels,” he adds.

How The Housing Market Benefits

Lower foreclosure rates are a positive for real estate, both nationally and in local markets.

“It’s good news that the market in most areas is not dealing with the uncertainty of a high share of distressed properties competing with regular sales,” notes Blomquist.

“This leads to a healthier and normal real estate ecosystem. Home prices are steadily rising over the long-term, and home builders are more confident to create extra supply without fear of having to compete with foreclosures.”

Ultimately, that should help restore balance to the supply-demand equation, he says.

Continue reading.

Recent Comments