by LLT | May 3, 2017 | LLT, News

For the first time in a decade, more new households chose to buy a home rather than rent one in the first quarter of 2017, according to Census Bureau data. About 854,000 new households purchased a home—more than double the 365,000 new households who chose to rent. New homeowners have not outpaced new renters since the third quarter of 2006.

For the first time in a decade, more new households chose to buy a home rather than rent one in the first quarter of 2017, according to Census Bureau data. About 854,000 new households purchased a home—more than double the 365,000 new households who chose to rent. New homeowners have not outpaced new renters since the third quarter of 2006.

The overall homeownership rate in the first quarter of 2017 was 63.6 percent, down slightly from 63.7 percent in the fourth quarter of 2016. But economists say the increase in new households who purchased could signal a turnaround in the long-term decline of the overall homeownership rate, according to The Wall Street Journal.

In the mid-2000s, the homeownership rate peaked at about 69 percent. In the second-quarter of 2016, it hit a 50-year low of 62.9 percent but has been gradually climbing since then. “People are looking at housing as being a bit more attractive, as memories of the financial crisis fade,” Joseph LaVorgna, chief U.S. economist at Deutsche Bank, told the Journal.

Indeed, existing-home sales zoomed to their strongest sales pace in a decade in March, according to the National Association of REALTORS®. New-home sales also edged up 5.8 percent in March.

Read the full article.

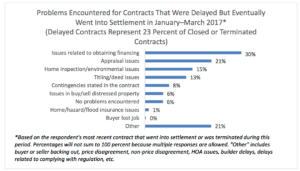

by LLT | May 2, 2017 | LLT, News

Fewer respondents cite financing as an issue today than when the survey began tracking such data

Twenty-three percent of real estate professionals say they faced closing delays for a transaction in March, and 7 percent say the sale contract was terminated altogether, according to the REALTORS® Confidence Index, which is based on responses from more than 2,500 REALTORS® nationwide. Clients who had trouble obtaining financing was the most common reason for delays, respondents to the survey say, followed by appraisal issues.

Though it remains the top roadblock to closing, fewer respondents cite financing as an issue today than when the survey began tracking such data. “The decline may reflect the improvement in the economic environment, better credit histories from borrowers, and improvement in the loan evaluation processes of mortgage originations,” the report notes.

But appraisal issues are growing more common. Real estate practitioners say a shortage of appraisers, valuations that are not in line with market conditions, and “out-of-town” appraisers who are not familiar with the local market are the biggest problems they face concerning appraisals. Indeed, 55 percent of mortgage originators recently surveyed reported some level of difficulty getting appraisals, according to a separate NAR survey.

Read the full article.

by LLT | Apr 27, 2017 | LLT, News

-

Total mortgage application volume rose 2.7 percent last week, according to the Mortgage Bankers Association.

Total mortgage application volume rose 2.7 percent last week, according to the Mortgage Bankers Association.

-

Volume was 18 percent lower compared with the same week one year ago.

The refinance market came back to life last week, as mortgage rates fell further. Homebuyers, however, were not as easily swayed by rates.

Total mortgage application volume rose 2.7 percent, seasonally adjusted, for the week, according to the Mortgage Bankers Association. Volume was 18 percent lower compared with the same week one year ago.

Mortgage refinance volume remains far weaker than it was last year, when interest rates were lower, but it did rise 7 percent week to week as rates sank to the lowest level since just after following the presidential election. The size of the average refinance loan also increased, as large-balance borrowers are more rate sensitive. Refinances are still 34 percent below where they were a year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances of $424,100 or less decreased to 4.20 percent from 4.22 percent, with points increasing to 0.37 from 0.35, including the origination fee, for 80 percent loan-to-value ratio loans.

“The drop was driven by continued investor concerns about the French election, though Sunday’s first-round voting results apparently have alleviated some investor fears,” said Lynn Fisher, MBA vice president of research and economics.

Homebuyers were less concerned with mortgage rates and more frustrated with the lack of homes for sale. Mortgage applications to purchase a home fell 1 percent for the week and are just 0.4 percent higher than the same week last year. The supply of homes for sale continues to drop amid strong demand and low production from the nation’s homebuilders.

Mortgage rates may eventually become a bigger concern. They began rising again this week, as investors turned from the French election to the possibility of U.S. tax reform.

“In general, investors have piled back into riskier assets like stocks because the French election reduces long-term risks to the European Union,” said Matthew Graham, chief operating officer of Mortgage News Daily. “The prospects for tax reform have a similar effect in that they encourage investors to favor riskier assets at the expense of bonds. When demand for bonds decreases relative to supply, rates move higher.”

Read the full article.

by LLT | Apr 26, 2017 | LLT, News

The inventory squeeze has left home buyers with fewer options on the market than they’ve seen in decades. While that’s bad news for them, the continuously high demand means it’s one of the best times to be a seller—ever.

The inventory squeeze has left home buyers with fewer options on the market than they’ve seen in decades. While that’s bad news for them, the continuously high demand means it’s one of the best times to be a seller—ever.

“I’ve been selling real estate for 25 years, and this is the strongest seller’s market I have ever seen in my entire real estate career,” David Fogg, a sales associate with Keller Williams Realty World Media Center in Burbank, Calif., told CNBC. “A lot of our sellers are optimistically pricing their homes in today’s market, and I have to say, in most cases, we’re getting the home sold anyway.” He says he recently listed what’s considered an entry-level home in the area—a three-bedroom, two-bath, 1,240-square foot home—for $789,000. The seller received three offers before Fogg held the first open house, which 100 would-be buyers attended.

“It’s very tough. Most of the listings are intentionally listed a little low to get a lot of attention, and it’s not uncommon to get 12 to 16 offers on one property,” says Jilbert Mosessian, a renter in the Burbank area who is looking to buy a home. He says he recently put offers on three homes considerably higher than their listing prices, “and I was told that there were still five people above me and [the seller was] only going to deal with them.”

The inventory of homes for sale decreased by 6.6 percent at the end of March compared to a year ago, according to the National Association of REALTORS®. Unsold housing inventory is at a 3.8-month supply. Most economists consider a balanced market to be a five- to six-month supply. Forty-eight percent of homes in March sold in less than a month.

To better compete, buyers are dropping contingencies and offering more cash down. Real estate professionals also are bracing their clients for potential appraisal issues because in hot markets, homes may appraise below the bid-up sale price.

Continue reading.

by LLT | Apr 25, 2017 | LLT, News

Down from 47 days this time last year

Down from 47 days this time last year

Forty-eight percent of homes sold in March were on the market for less than a month, according to housing data from the National Association of REALTORS®. The average for all sold properties, though, was a little higher, at 34 days. Still, that’s down significantly from 47 days a year ago, according to NAR. Nondistressed homes spent a median of 32 days on the market, which is the shortest length of time since NAR began tracking such data in May 2011.

Realtor.com® reveals that the following metro areas had listings on the market the shortest amount of time in March:

- San Jose-Sunnyvale-Santa Clara, Calif.: 24 days

- San Francisco-Oakland-Howard-Hayward, Calif.: 25 days

- Seattle-Tacoma-Bellevue, Wash.: 28 days

- Denver-Aurora-Lakewood, Colo.: 28 days

- Vallejo-Fairfield, Calif.: 31 days

With strong buyer demand supporting shorter times on market, home prices are rising as well. The median existing-home price for all housing types was $236,400 in March, up 6.8 percent from a year ago. “Last month’s swift price gains and the remarkably short time a home was on the market are directly the result of the homebuilding industry’s struggle to meet the dire need for more new homes,” says NAR chief economist Lawrence Yun. “A growing pool of all types of buyers is competing for the lackluster amount of existing homes on the market. Until we see significant and sustained multi-month increases in housing starts, prices will continue to far outpace incomes and put pressure on those trying to buy.”

Read the full article.

by LLT | Apr 24, 2017 | LLT, News

Home sales are predicted to decline from record highs in 2016, according to Freddie Mac.

Home sales are predicted to decline from record highs in 2016, according to Freddie Mac.

Prospective homebuyers should expect to shell out more as home prices are going beyond the boundaries of income and as interest rates are increasing.

“Tight housing inventory has been an important feature of the housing market at least since 2016. For-sale housing inventory, especially of starter homes, is currently at its lowest level in over ten years,” said Freddie Mac Chief Economist Sean Becketti. “If inventory continues to remain tight, home sales will likely decline from their 2016 levels. As we enter the spring home buying season, all eyes are on housing inventory and whether or not it will meet the high demand.”

Many homeowners currently feel uneasy in selling their homes due to fear that they won’t be able to find another home they like that’s in their budget, according to Freddie Mac. “fear of not being able to find another home they like and that falls within their budget” and not wanting to let go of their current low mortgage rates are the reasons Freddie Mac cited for low for-sale housing inventory.

Total home sales are forecasted to be at 5.90 million this year and 6.02 million in 2018; house prices are expected to grow by 5.2% this year and 4.1% next year; and total originations are projected at $1.545 billion this year and $1.5 billion next year.

Read the full article.

For the first time in a decade, more new households chose to buy a home rather than rent one in the first quarter of 2017, according to Census Bureau data. About 854,000 new households purchased a home—more than double the 365,000 new households who chose to rent. New homeowners have not outpaced new renters since the third quarter of 2006.

For the first time in a decade, more new households chose to buy a home rather than rent one in the first quarter of 2017, according to Census Bureau data. About 854,000 new households purchased a home—more than double the 365,000 new households who chose to rent. New homeowners have not outpaced new renters since the third quarter of 2006.

Recent Comments