Mortgage payments make up the biggest chunk of U.S. homeowners’ income since 2010.

The average monthly mortgage payment made up 15.8% of buyers’ income in the fourth quarter of last year, according to real estate website Zillow, the biggest share of homeowner income since the second quarter of 2010, thanks to rising interest rates and increasing home values. The average monthly payment was $758 at the end of last year, up from $690 in 2015. Though it’s still not quite as bad as the national average of 21% between 1985 to 2000. “This is a phenomenon that really affects homebuyers a whole lot more,” said Svenja Gudell, chief economist at Zillow.

Affording a house will get a lot harder next year, and because banks have tightened restrictions on mortgage lending, some people aren’t even trying to apply for mortgages. People with low credit scores are especially at a disadvantage, as lenders have tougher expectations for borrowers to meet — the third quarter of 2016 saw the highest quality home loans since 2000, but that means those applying must have stellar credit scores (the average for loans originating in the third quarter of last year was 739).

But it could be worse, and in some cities, it is. Coastal cities see even higher shares of their income go toward their mortgages. In New York, for example, homeowners spent 27% of their income on their mortgage payments, and in San Francisco, it was more than 42%. There is one bright spot for those who have already bought homes: Current homeowners would obviously only be affected by rising interest rates if they chose an adjustable-rate mortgage, which fluctuates as opposed to a fixed-rate, Gudell said.

In general, the rule of thumb for buying a home is to spend no more than three times your income — so if you make $100,000, you should look for a house that costs about $300,000, Gudell said. It’s a rough estimate, and likely doesn’t apply to homes on the country’s coasts, in places like Los Angeles and New York.

Your monthly housing payment, including your principal, interest, taxes, insurance and in co-op and condo situations, home association fees, should not take up more than 28% of your salary before taxes, according to estimates by personal finance site Bankrate.com.

Distressed Homes Drag Down The Neighborhood Home Prices

Homeowners don’t like to see abandoned houses on their block. Zombie foreclosures—vacated homes that have yet to complete the foreclosure process—can be more than an eyesore. They may also attract crime and lower surrounding home prices.

If you’re shopping for a mortgage loan and a home, there’s good news on this front. Foreclosure rates are falling fast.

What New Data Reveal

Fresh numbers from ATTOM Data Solutions show that foreclosure activity nationally plunged to a 10-year low in 2016. Looking closer, U.S. foreclosure rates dropped by 30 percent last year.

That’s the most improvement of any year on record, according to Black Knight Financial Services. December 2016’s 59,700 foreclosure starts marked an amazing 24 percent decrease from the same period a year earlier.

Foreclosure filings surpassed 2.8 million in 2010. Last year, they tallied 933,045. That’s a sign that the housing market is in much better shape today than a few years ago.

Why Foreclosures Are Down

Daren Blomquist, senior vice president for ATTOM Data Solutions, says foreclosure filings are down for two reasons.

First, since the last housing bubble, there are fewer “legacy” foreclosures—meaning homes in the foreclosure process with loans originated between 2004 and 2008.

“Most legacy foreclosures have either been already foreclosed on or resolved in some other way, such as refinancing, modification or short sale,” says Blomquist.

Second, “loans originated over the past seven years are holding up well, with default rates below historically normal levels,” he adds.

How The Housing Market Benefits

Lower foreclosure rates are a positive for real estate, both nationally and in local markets.

“It’s good news that the market in most areas is not dealing with the uncertainty of a high share of distressed properties competing with regular sales,” notes Blomquist.

“This leads to a healthier and normal real estate ecosystem. Home prices are steadily rising over the long-term, and home builders are more confident to create extra supply without fear of having to compete with foreclosures.”

Ultimately, that should help restore balance to the supply-demand equation, he says.

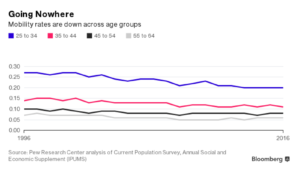

Fairly or not, the generation of millennials has a reputation as footloose and fancy-free.

Or, to put it less kindly, millennials are slow to launch—slower to get married, buy a house, and have kids than the young people of previous generations.

So you’d think they’d be moving all over the country, discovering whether they’d rather live in a micro-apartment in the Midwest, say, or telecommute from an old farmhouse a couple of hours outside a big city.

But it’s not just young people. The share of the population that has moved at least once within the past year, a key measure of mobility, has followed the same trend among other cohorts of the working population, as the chart below shows.

It may be that the job market is weaker today, at least in parts of the country, than the national unemployment numbers say, Fry said. Or it may be that millennials are frozen in place by a housing market that’s still short of supply to meet the demand. Under that theory, older homeowners aren’t trading up for more expensive homes, choosing instead to remain in cheaper models, thereby limiting the number of starter homes on the market.

Mobility is important to the economy. People who move spend money on houses, furniture, real estate agents, and moving companies. People moving to pursue a job are often seen as a sign of a healthy economy.

Fry didn’t have data handy for every age cohort, but he did pull figures for the 25-35 group. In 2000, when that group was made up of Gen Xers, 50 percent of respondents said they moved for housing-related reasons, like wanting to own or to live in a nicer neighborhood. Meanwhile, 21 percent of that age group moved for job-related reasons in 2000.

Federal Reserve Chair Janet Yellen prepares to speak before a Senate Banking, Housing, and Urban Affairs Committee hearing on the “Semiannual Monetary Policy Report to the Congress” on Capitol Hill in Washington, U.S., February 14, 2017. REUTERS/Joshua Roberts

The Federal Reserve will likely need to raise interest rates at an upcoming meeting, Fed Chair Janet Yellen said on Tuesday, although she flagged considerable uncertainty over economic policy under the Trump administration.

Yellen said delaying rate increases could leave the Fed’s policymaking committee behind the curve and eventually lead it to hike rates quickly, which she said could cause a recession.

“Waiting too long to remove accommodation would be unwise,” Yellen told the U.S. Senate Banking Committee, citing the central bank’s expectations the job market will tighten further and that inflation would rise to 2 percent.

“At our upcoming meetings, the committee will evaluate whether employment and inflation are continuing to evolve in line with these expectations, in which case a further adjustment of the federal funds rate would likely be appropriate.”

Yellen did not say if Fed policymakers expected the economy would warrant three interest rate increases this year, as they last signaled in December. Nor did she give indications whether the first rate hike of the year might come at its next meeting in March or at the June meeting, which is when most analysts expect a rate increase.

“I can’t tell you which meeting it would be,” she said, including specifying “whether it’s March or May or June.”

Since the end of the 2007-09 recession, the Fed has raised rates once in December 2015 and again in December of last year.

Yellen added that Fed policymakers would be discussing in the coming months how the central bank will eventually reduce the size of its bond portfolio, which ballooned during the financial crisis as the Fed sought to keep rates low. She repeated the Fed’s guidance that reducing its holdings would begin when the Fed’s current cycle of rate hikes is well under way.

Yellen was appearing in Congress for the first time since Republicans took control of the White House and both houses of the legislature and she nodded to the uncertainties over the direction of U.S. economic policy.

“Changes in fiscal policy or other economic policies could potentially affect the economic outlook,” she said. “It is too early to know what policy changes will be put in place or how their economic effects will unfold.”

The Iron Horse had brass fixtures in his house. And galvanized steel wiring. He also had clapboard siding, parquet floors and a screened-in porch.

Lou Gehrig, the Yankee’s iconic first baseman, bought the home in New Rochelle, N.Y., in December 1927, just two months after completing one of the most successful seasons any major league hitter has ever had, culminating in a World Series title. He then refurbished the three-bedroom structure to accommodate both himself and his parents, taking great care to turn it into a place they would all feel proud to call home.

But today the old house, while still maintaining some of Gehrig’s handwork, sits cold and neglected, in search of a new owner.

Arthur Scinta, a local preservationist and architectural historian, hopes the house, 13 miles north of Yankee Stadium, can be restored and preserved in the style in which Gehrig fashioned it, perhaps even turned into a Lou Gehrig museum.

“You can still feel Gehrig’s presence in the house,” Scinta said. “It would be a shame if all that was lost.”

But the house, it turns out, also has a puzzling history – specifically, it was foreclosed on in 1937 while Gehrig’s parents, Christina and Heinrich, still owned it.

Gehrig bought the house, at 9 Meadow Lane, in his mother’s name, taking over an existing mortgage of $10,000, according to 1927 records. Gehrig and his parents then moved in shortly after Christmas, with Gehrig working hard to fix it up to his liking.

“Not a bad joint, is it?” he was quoted in a story published in The New York Sun on Jan. 9, 1928. “Not a new place, but it will be as good as new when I get ‘er all dolled up. It was a Christmas gift to my mother.”

Gehrig, whose appearance in 2,130 consecutive games earned him the nickname the Iron Horse, is described in the Sun story as being covered in paint and plaster as he worked on the house. He lived there, with his parents, until he moved out in 1933 after marrying Eleanor Twitchell. In all, Gehrig won two World Series titles while residing at that address. Another local newspaper described him playing ball with local children across the street.

Mortgage payments make up the biggest chunk of U.S. homeowners’ income since 2010.

Mortgage payments make up the biggest chunk of U.S. homeowners’ income since 2010.

Recent Comments