by LLT | May 15, 2017 | LLT, News

-

Figures support idea that recent slowdown was transitory

Figures support idea that recent slowdown was transitory

-

Michigan consumer-sentiment gauge ticks up to four-month high

The U.S. economy is back on track for steady growth, though not much more.

Data released Friday showed consumer retail purchases rose last month, albeit less than forecast, after a March gain that was revised from a decline, indicating the early-2017 slowdown was transitory. The consumer-price index stabilized in April following the first drop in a year, though a gauge excluding food and energy posted the smallest year-over-year increase since October 2015.

The pickup in retail sales — with gains in nine of 13 major categories — eases concern from earlier in the year about a loss of momentum in household spending, the biggest part of the economy. The CPI results are a reminder that while businesses are regaining some pricing power, inflation is hardly breaking out.

Together, the data indicate progress consistent with the Federal Reserve’s view of the economy and inflation ahead of policy makers’ mid-June meeting, where they are widely expected to continue their gradual pace of interest-rate increases with a quarter-point hike. The Fed may feel less pressure, however, to pick up the pace should core inflation remain subdued.

“It’s a pretty decent overall picture of the U.S. economy,” said Sal Guatieri, a senior economist at BMO Capital Markets in Toronto. “Consumer spending is rebounding, though possibly not as much as we expected. On the inflation front, there’s not a lot of pricing pressure, and it looks like inflation is gravitating toward the Fed’s goal.”

A separate report showed that the University of Michigan consumer confidence index climbed to a four-month high in May, and within that, buying conditions for large household durables rose to the highest since 2005, reinforcing signs that Americans remain optimistic about spending.

“Today’s sub-consensus U.S. data is unlikely to rock the Fed’s boat, meaning there are increasingly few reasons for not hiking in June,” James Smith, an economist at ING in London, wrote in a note.

Continue reading.

by LLT | May 10, 2017 | LLT, News

-

Mortgage application volume is still nearly 14 percent below year-ago levels because of weaker refinancing.

Mortgage application volume is still nearly 14 percent below year-ago levels because of weaker refinancing.

-

“Continuing strength in the job market and improving consumer confidence drove overall purchase applications to increase last week,” said economist Joel Kan.

The gains are slow and small, but mortgage volume is beginning to improve again, as more homebuyers sign on the dotted line.

Total mortgage application volume increased 2.4 percent on a seasonally adjusted basis last week from the previous week. Volume is still nearly 14 percent below year-ago levels because of weaker refinancing, according to the Mortgage Bankers Association .

Even as buyers complain of high home prices and limited listings, mortgage applications to purchase a home gained 2 percent for the week and are 6 percent higher than a year ago.

“Continuing strength in the job market and improving consumer confidence drove overall purchase applications to increase last week,” said MBA economist Joel Kan. “The index for purchase applications reached its highest level since the beginning of October 2015, which was the week prior to the implementation of the federal government’s ‘know before you owe’ rule.”

That rule had lenders concerned that compliance would delay the mortgage process, which it did for a short time. Demand for mortgages was likely high just prior to its implementation, as buyers rushed to get in and avoid those delays.

Mortgage applications to refinance a home loan rose 3 percent for the week but are still 32 percent below last year, when interest rates were lower.

The average contract interest rate for 30-year fixed rate mortgages with conforming loan balances of $424,100 or less remained unchanged at 4.23 percent, with points decreasing to 0.31 from 0.32, including the origination fee, for 80 percent loan-to-value ratio loans.

Mortgage rates have been inching higher in general and have only moved lower on three out of the past 15 business days, according to Mortgage News Daily.

“While that sort of losing streak sounds fairly unpleasant, the size of the movement has been far from threatening,” said Matthew Graham, Mortgage News’ chief operating officer.

Continue reading.

by LLT | May 8, 2017 | LLT, News

Fed Funds Rate to level out at 3%

Fed Funds Rate to level out at 3%

The Congressional Budget Office, which provides nonpartisan analysis for the U.S. Congress, released its 2017 Budget and Economic Outlook, which showed a forecasted nine federal funds rate hikes by the year 2020.

Wednesday, the Federal Open Markets Committee met, deciding not to raise rates again after having just raised them in the March meeting. However, housing experts explainedthat recent economic data supports the consensus that the Fed will raise rates in December and once more in 2017.

The CBO released a chart that shows interest rates will rise steadily, probably about three rate hikes of 25 basis points per year, and finally level out at 3% in 2020.

The current target range for the federal funds rate stands at .75% to 1%. The chart shows once the federal funds rate hits 3% in 2020, it will hold that pace for several years, remaining at 3% at least until 2027.

While 3% is a significant increase from today’s rate, the chart shows it is still substantially lower than the pre-crisis years between 2002 and 2007.

Read the full article.

by LLT | May 3, 2017 | LLT, News

For the first time in a decade, more new households chose to buy a home rather than rent one in the first quarter of 2017, according to Census Bureau data. About 854,000 new households purchased a home—more than double the 365,000 new households who chose to rent. New homeowners have not outpaced new renters since the third quarter of 2006.

For the first time in a decade, more new households chose to buy a home rather than rent one in the first quarter of 2017, according to Census Bureau data. About 854,000 new households purchased a home—more than double the 365,000 new households who chose to rent. New homeowners have not outpaced new renters since the third quarter of 2006.

The overall homeownership rate in the first quarter of 2017 was 63.6 percent, down slightly from 63.7 percent in the fourth quarter of 2016. But economists say the increase in new households who purchased could signal a turnaround in the long-term decline of the overall homeownership rate, according to The Wall Street Journal.

In the mid-2000s, the homeownership rate peaked at about 69 percent. In the second-quarter of 2016, it hit a 50-year low of 62.9 percent but has been gradually climbing since then. “People are looking at housing as being a bit more attractive, as memories of the financial crisis fade,” Joseph LaVorgna, chief U.S. economist at Deutsche Bank, told the Journal.

Indeed, existing-home sales zoomed to their strongest sales pace in a decade in March, according to the National Association of REALTORS®. New-home sales also edged up 5.8 percent in March.

Read the full article.

by LLT | May 2, 2017 | LLT, News

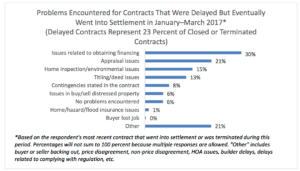

Fewer respondents cite financing as an issue today than when the survey began tracking such data

Twenty-three percent of real estate professionals say they faced closing delays for a transaction in March, and 7 percent say the sale contract was terminated altogether, according to the REALTORS® Confidence Index, which is based on responses from more than 2,500 REALTORS® nationwide. Clients who had trouble obtaining financing was the most common reason for delays, respondents to the survey say, followed by appraisal issues.

Though it remains the top roadblock to closing, fewer respondents cite financing as an issue today than when the survey began tracking such data. “The decline may reflect the improvement in the economic environment, better credit histories from borrowers, and improvement in the loan evaluation processes of mortgage originations,” the report notes.

But appraisal issues are growing more common. Real estate practitioners say a shortage of appraisers, valuations that are not in line with market conditions, and “out-of-town” appraisers who are not familiar with the local market are the biggest problems they face concerning appraisals. Indeed, 55 percent of mortgage originators recently surveyed reported some level of difficulty getting appraisals, according to a separate NAR survey.

Read the full article.

Recent Comments