by LLT | Mar 7, 2017 | LLT, News

Housing data in January gave mixed signals on the direction for the year. Closing activity for existing home sales shot up to a decade-high of 5.69 million units at an annualized pace, but pending contracts fell to their lowest level in 12 months. For the whole of 2017, I expect existing home sales to reach 5.6 million, which would be a gain of 2.2% from the prior year, but below the annualized pace set in January. In short, expect sideway movements for the rest of the year.

Housing data in January gave mixed signals on the direction for the year. Closing activity for existing home sales shot up to a decade-high of 5.69 million units at an annualized pace, but pending contracts fell to their lowest level in 12 months. For the whole of 2017, I expect existing home sales to reach 5.6 million, which would be a gain of 2.2% from the prior year, but below the annualized pace set in January. In short, expect sideway movements for the rest of the year.

Even though home sales will not make much gains, home prices will. With inventories still at grossly inadequate levels, there is only one direction to go for home prices. The national median price will likely rise by 4% to 5%. Do not be surprised if it goes up even higher. While the country needs around 1.6 million new housing starts, only around 1.3 million units will be constructed, based on permit information and from labor and lot shortages facing the industry.

For local markets, check how new home construction is coming online in relation to local job growth to gauge if home prices will outpace the national average growth rate. For example, in Savannah, Georgia, there have been only 6,000 new units built cumulatively over the past three years while 18,000 net new jobs have been added. Historically, one new housing unit is required for every two new jobs. Therefore, demand is outpacing supply there and home price outlook is solid in Savannah.

Though there are many short-term factors and dynamics at play, it is also worthwhile to gauge what is likely to happen over the long-term. Specifically, housing demand over the next decade will be notably higher than it is now. The combined factors of a rising population and jobs with the release of the pent-up demand will be the principal drivers.

Continue reading.

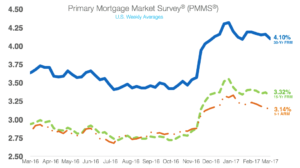

by LLT | Mar 6, 2017 | LLT, News

30-year mortgage rate holds relatively steady in 2017

30-year mortgage rate holds relatively steady in 2017

Mortgage rates broke their month-long holding pattern as they decreased this week, according to Freddie Mac’s Primary Mortgage Market Survey.

“Since the beginning of the year, the 10-year Treasury yield has covered a 22 basis-point range,” Freddie Mac Chief Economist Sean Becketti said. “The range of movement for the 30-year has been half that, just 11 basis points.”

The 30-year fixed rate mortgage decreased to 4.1% for the week ending March 2, 2017. This is down from last week’s 4.16% but still up from last year’s 3.64%.

The 15-year FRM also dropped to 3.32%, down from last week’s 3.37% but still up from last year’s 2.94%.

The five-year Treasury-indexed hybrid adjustable-rate mortgage decreased slightly to 3.14%, down from 3.16% last week. This is up from 2.84% last year.

“The 10-year Treasury yield remained relatively flat this week, while the 30-year mortgage rate fell six basis points to 4.1%,” Becketti said.

Read the full article.

by LLT | Mar 3, 2017 | LLT, News

Deed restrictions can bring nasty surprises to homeowners looking to remodel or even when buying a home. These restrictions can limit a number of property features, such as the number of bedrooms in your home, the building height, the type of vehicles in your driveway, the fencing permitted, the type and number of trees that can be removed from a property, and even the style and color of construction materials used in a renovation (which often is intended to limit architectural variations in a neighborhood).

Deed restrictions can bring nasty surprises to homeowners looking to remodel or even when buying a home. These restrictions can limit a number of property features, such as the number of bedrooms in your home, the building height, the type of vehicles in your driveway, the fencing permitted, the type and number of trees that can be removed from a property, and even the style and color of construction materials used in a renovation (which often is intended to limit architectural variations in a neighborhood).

Be sure to make your clients aware of any deed restrictions—often called “restrictive covenants”—before they buy to avoid problems later on. The property does not have to be part of a homeowners association to be limited by a developer rule included in a deed.

“Deed restrictions turn up during title searches and a careful reading of the current deed,” a realtor.com® article notes. Anyone who buys the property must abide by the restrictions, even if they were put in place on the land a century ago. Deed restrictions are known for being difficult to change and often take a judicial ruling to invalidate them.

“When building a new home, or even doing an addition to your current home, it’s vital that you check your deed for any building restrictions,” says Bill Golden, a real estate professional in Atlanta.

Zachary D. Schorr, a Los Angeles real estate attorney, told realtor.com® that he’s seen deed restrictions run the gamut, such as those that required exterior paint colors to match colors found in nature to those that restricted rental properties.

“With the rise of VRBO and Airbnb, we are even seeing restrictions on nightly rentals and the minimum rental period for a house,” Schorr says.

Read the full article.

by LLT | Mar 2, 2017 | LLT, News

Treasury Secretary Steven Mnuchin speaks at a press briefing at the White House in Washington, U.S., February 14, 2017. REUTERS/Kevin Lamarque

U.S. Treasury Secretary Steven Mnuchin said on Wednesday the Trump administration’s tax reform plan will not change the deductibility of mortgage interest and charitable contributions.

“Let me first clarify, we are not taking away the charitable deduction and we are leaving the mortgage interest deduction as is,” Mnuchin said in an interview on Fox Business Network.

“We think those are both very, very important. But what we are going to do is we are looking at other things where the reduction in deductions will offset the rate,” he said.

On Dec. 1, prior to President Donald Trump taking office, Mnuchin told CNBC that Trump wanted to cap the amount of mortgage interest that taxpayers can deduct.

The mortgage interest deduction is already capped at loans up to $1 million if you are married and filing income taxes jointly, and at $500,000 if you file separately.

Trump, in a speech to Congress on Tuesday night, said he wanted to provide “massive tax relief” to the middle class and cut corporate tax rates, but he did not offer specifics.

Mnuchin said he expects a tax reform plan to be passed by Congress and signed by the president by August.

Trump has said tax reform should reduce tax rates for individuals and businesses, do away with longstanding tax loopholes and broaden the tax base in order to drive U.S. economic growth.

Read the full article.

by LLT | Mar 1, 2017 | LLT, News

More than 1 in 3 mortgages has a “major impact” on the borrower’s ability to save. That number jumps to 51 percent for parents who have mortgages.

More than 1 in 3 mortgages has a “major impact” on the borrower’s ability to save. That number jumps to 51 percent for parents who have mortgages.

That’s according to Bankrate’s Money Pulse survey for February.

Mortgages affect savings

Asked, “How much of an impact does the size of your mortgage have on your ability to save money for the future?” 37 percent of respondents said their mortgage has a major impact. Another 46 percent said it has a minor impact on savings.

There was a big split between parents of children under 18 and everyone else: 51 percent of the parents with children said their mortgage has a major impact on savings, and 27 percent of everyone else said their mortgage has a major impact on savings.

“It’s probably not as much about the mortgage as it is that stage of life,” says Jonathan Smoke, chief economist for Realtor.com.

Homeowners with children are likely to be in their early 30s to their mid-50s, with competing financial goals: Keeping the kids clothed and fed and educated, saving for college, saving for retirement, paying the mortgage, maintaining the home.

Jim Sahnger, mortgage planner for Schaffer Mortgage in Palm Beach Gardens, Florida, recommends thinking of a mortgage payment as a form of savings.

“If you look at it from the aspect of you’re building equity, that’s obviously important,” he says.

Homeownership also shelters you from rent hikes and it might convey tax benefits, he says.

The homebuying age

Other results from the survey:

- 15 percent of Americans say they’re very or somewhat likely to buy a home this year.

- Older millennials and Gen Xers are the most likely to be in the market for a home.

- Among parents who don’t own homes, 2 in 3 say financial issues prevent them from buying.

Who is very or somewhat likely to buy a home this year? Here’s the age breakdown:

- Younger millennials (ages 18-26): 15 percent

- Older millennials (ages 27-36): 20 percent

- Gen Xers (ages 37-52): 20 percent

- Baby boomers (ages 53-71): 11 percent

- Silent Generation (72 and older): 4 percent

This doesn’t surprise Smoke at all. The dominant homebuying segment is people ages 25 to 34.

Regardless of generational labels, “if you had history going back 50 years, you would see this pattern is true in both good times and bad,” Smoke says.

People often buy their first homes shortly before or after children are born.

Kevin Hartman fits the pattern.

When he and his wife bought their first house, “I was 29 when we closed and not even a year back from my first deployment to Iraq. I was married to Andrea and we were pregnant with our first baby girl at the time. All three of our kids were born while we lived in that home since we lived there for six years.”

They sold that house in Salem, Oregon, a couple of years ago, and just bought a town house in Portland, Oregon.

Continue reading.

by LLT | Feb 28, 2017 | LLT, News

Billionaire and renowned investor Warren Buffett has seen mammoth appreciation for a getaway home he owns in Laguna Beach, Calif. He purchased it in 1971 for $150,000. Now Buffett is selling the six-bedroom, 6.5-bath home for $11 million.

Billionaire and renowned investor Warren Buffett has seen mammoth appreciation for a getaway home he owns in Laguna Beach, Calif. He purchased it in 1971 for $150,000. Now Buffett is selling the six-bedroom, 6.5-bath home for $11 million.

Are there any lessons from Buffett’s savvy investment that others can draw from who are looking for high appreciation over time? Realtor.com® spotlights a few.

Distinguish between price and value.

Buffett first bought the home in Laguna Beach not as an investment but simply because his wife liked the home. And he still paid top dollar for it. The equivalent of $150,000 in 1971 is nearly $900,000 today, according to the Bureau of Labor Statistics’ inflation calculator. “While the town may have been no big deal at the time, the home’s nice layout and its proximity to the beach and to Los Angeles clearly offered value,” realtor.com®’s article notes.

Buy and hold.

Buffett shared some of his best investing advice with shareholders of his company, Berkshire Hathaway Inc., in 1989: “Time is the friend of the wonderful business, the enemy of mediocre.” Time in real estate tends to be on an owners’ side. Buy and hold property for, say, 46 years and you’re likely to see some appreciation (and pay off that 30-year mortgage).

Stay up to date.

The Laguna Beach home was originally constructed in 1936. The Buffetts remodeled it several times over the years, taking the opportunity to spotlight some of the strongest sales points of the home as well. The Buffetts expanded the square footage of the home and added in views of the beach area from nearly every room in the home, says Bill Dolby, the listing agent with Villa Real Estate. They also added several decks, including an oversized viewing deck from the family room.

Buy what you want to own.

Buffett didn’t originally buy the house believing he was going to make a fortune from it at resale. He just wanted a getaway for his family and they liked the area. They’ve spent many vacations and summers there over four decades of ownership too. “Viewed that way, he’s more than gotten his money’s worth, regardless of the appreciation,” the realtor.com® article notes.

Read the full article.

Recent Comments