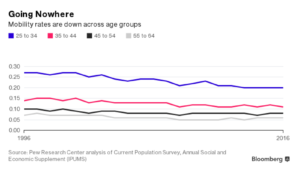

Fairly or not, the generation of millennials has a reputation as footloose and fancy-free.

Or, to put it less kindly, millennials are slow to launch—slower to get married, buy a house, and have kids than the young people of previous generations.

So you’d think they’d be moving all over the country, discovering whether they’d rather live in a micro-apartment in the Midwest, say, or telecommute from an old farmhouse a couple of hours outside a big city.

But it’s not just young people. The share of the population that has moved at least once within the past year, a key measure of mobility, has followed the same trend among other cohorts of the working population, as the chart below shows.

It may be that the job market is weaker today, at least in parts of the country, than the national unemployment numbers say, Fry said. Or it may be that millennials are frozen in place by a housing market that’s still short of supply to meet the demand. Under that theory, older homeowners aren’t trading up for more expensive homes, choosing instead to remain in cheaper models, thereby limiting the number of starter homes on the market.

Mobility is important to the economy. People who move spend money on houses, furniture, real estate agents, and moving companies. People moving to pursue a job are often seen as a sign of a healthy economy.

Fry didn’t have data handy for every age cohort, but he did pull figures for the 25-35 group. In 2000, when that group was made up of Gen Xers, 50 percent of respondents said they moved for housing-related reasons, like wanting to own or to live in a nicer neighborhood. Meanwhile, 21 percent of that age group moved for job-related reasons in 2000.

Federal Reserve Chair Janet Yellen prepares to speak before a Senate Banking, Housing, and Urban Affairs Committee hearing on the “Semiannual Monetary Policy Report to the Congress” on Capitol Hill in Washington, U.S., February 14, 2017. REUTERS/Joshua Roberts

The Federal Reserve will likely need to raise interest rates at an upcoming meeting, Fed Chair Janet Yellen said on Tuesday, although she flagged considerable uncertainty over economic policy under the Trump administration.

Yellen said delaying rate increases could leave the Fed’s policymaking committee behind the curve and eventually lead it to hike rates quickly, which she said could cause a recession.

“Waiting too long to remove accommodation would be unwise,” Yellen told the U.S. Senate Banking Committee, citing the central bank’s expectations the job market will tighten further and that inflation would rise to 2 percent.

“At our upcoming meetings, the committee will evaluate whether employment and inflation are continuing to evolve in line with these expectations, in which case a further adjustment of the federal funds rate would likely be appropriate.”

Yellen did not say if Fed policymakers expected the economy would warrant three interest rate increases this year, as they last signaled in December. Nor did she give indications whether the first rate hike of the year might come at its next meeting in March or at the June meeting, which is when most analysts expect a rate increase.

“I can’t tell you which meeting it would be,” she said, including specifying “whether it’s March or May or June.”

Since the end of the 2007-09 recession, the Fed has raised rates once in December 2015 and again in December of last year.

Yellen added that Fed policymakers would be discussing in the coming months how the central bank will eventually reduce the size of its bond portfolio, which ballooned during the financial crisis as the Fed sought to keep rates low. She repeated the Fed’s guidance that reducing its holdings would begin when the Fed’s current cycle of rate hikes is well under way.

Yellen was appearing in Congress for the first time since Republicans took control of the White House and both houses of the legislature and she nodded to the uncertainties over the direction of U.S. economic policy.

“Changes in fiscal policy or other economic policies could potentially affect the economic outlook,” she said. “It is too early to know what policy changes will be put in place or how their economic effects will unfold.”

The Iron Horse had brass fixtures in his house. And galvanized steel wiring. He also had clapboard siding, parquet floors and a screened-in porch.

Lou Gehrig, the Yankee’s iconic first baseman, bought the home in New Rochelle, N.Y., in December 1927, just two months after completing one of the most successful seasons any major league hitter has ever had, culminating in a World Series title. He then refurbished the three-bedroom structure to accommodate both himself and his parents, taking great care to turn it into a place they would all feel proud to call home.

But today the old house, while still maintaining some of Gehrig’s handwork, sits cold and neglected, in search of a new owner.

Arthur Scinta, a local preservationist and architectural historian, hopes the house, 13 miles north of Yankee Stadium, can be restored and preserved in the style in which Gehrig fashioned it, perhaps even turned into a Lou Gehrig museum.

“You can still feel Gehrig’s presence in the house,” Scinta said. “It would be a shame if all that was lost.”

But the house, it turns out, also has a puzzling history – specifically, it was foreclosed on in 1937 while Gehrig’s parents, Christina and Heinrich, still owned it.

Gehrig bought the house, at 9 Meadow Lane, in his mother’s name, taking over an existing mortgage of $10,000, according to 1927 records. Gehrig and his parents then moved in shortly after Christmas, with Gehrig working hard to fix it up to his liking.

“Not a bad joint, is it?” he was quoted in a story published in The New York Sun on Jan. 9, 1928. “Not a new place, but it will be as good as new when I get ‘er all dolled up. It was a Christmas gift to my mother.”

Gehrig, whose appearance in 2,130 consecutive games earned him the nickname the Iron Horse, is described in the Sun story as being covered in paint and plaster as he worked on the house. He lived there, with his parents, until he moved out in 1933 after marrying Eleanor Twitchell. In all, Gehrig won two World Series titles while residing at that address. Another local newspaper described him playing ball with local children across the street.

As businesses evolve in the digital era, it’s affecting their needs when it comes to physical space in commercial properties. Broker-owners of commercial firms should take note of three trends Transwestern recently highlighted in its first quarter Insights report covering the retail, industrial, and multifamily sectors.

1. Retail: The Rise of Mobile Data

Retailers are getting more sophisticated in how they’re collecting mobile data about their customers. Many businesses are using mobile apps coupled with monitoring devices in their stores to track and interact with customers. If a consumer has that business’s app on their phone, it allows the retailers to engage with them by offering coupons or product suggestions. This personalized the shopping experience provides specialized data on consumer activity and interactions with the physical store location, according to Transwestern. This is influencing business owners’ location decisions and physical configuration needs at the storefront site.

2. Industrial: New Demands for E-Commerce Distribution Centers

Demands for faster shipments in online sales, and massive increases in e-commerce business is causing companies that have large fulfillment centers to rethink location. Previously, these online retailers chose industrial warehouses in lower cost areas outside of population centers. Today, there is a new demand for large commercial space closer to metro areas in order to more quickly and efficiently store and ship commodities to customers, according to Transwestern. These companies are seeking better access to various modes of transportation, such as trucks, rail, airfreight, and even seaports, So, real estate pros should identify sites with access to these amenities, as well as spaces that offer specific productivity and operation efficiencies that will help clients increase net operating income.

3. Multifamily:Micro-Unit Apartments in Urban Markets

As renters flock to urban centers for the live-work-play lifestyle, entry-level lease rates are becoming unaffordable for many recent college graduates, service workers, and young professionals, according to Transwestern. One way of providing more affordable living space is through micro-unit apartments. The Indie Apartments in Austin, Texas, for example, includes 138 apartments with 350-square-foot studios and 520-square-foot, two-bedroom units, and commercial restaurant space on the ground floor.

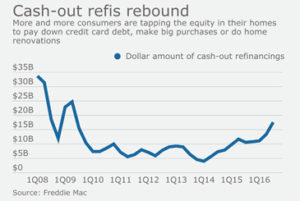

The surge in home values is good news for homeowners looking to tap the equity in their homes to pay down debt or make big purchases, but consumer advocates worry that it may be setting the stage for a spike in loan defaults.

Consumers have plenty of reasons to tap into their home equity, such as paying off credit card debt or financing long-delayed home-improvement projects. Banks are happy to oblige, especially with rising interest rates suppressing demand for traditional mortgage refinancing.

The problem is that a cash-out refi is much riskier than a credit card loan, said Sarah Wolff, a senior researcher at the Center for Responsible Lending.

“You are trading your unsecured debt for debt that’s tied to your home, and a default in that case would be much more catastrophic,” she said.

Banks are already seeing increased demand for cash-out refis. The total dollar amount of home equity cashed out rose 66% to $17.6 billion in the third quarter compared to the same period in 2015, according to Freddie Mac. The trend shows little sign of slowing down, said Len Kiefer, deputy chief economist at Freddie Mac.

“We expect overall volume of cash-out refis to trend higher,” Kiefer said.

Other lenders have placed bets recently that variations on the cash-out refinance model could catch fire with consumers. SoFi and Fannie Mae in November introduced a cash-out refi option specifically for paying down student loan debt.

Still, the overall industry level of cash-out refi volume remains at extremely low levels, even after a recent period of recovery, Kiefer said. The total dollar value of cash-out refis remained below $10 billion for several years during the recession. They have slowly inched back up, but remain well below pre-crisis levels of $30 billion and higher, so banks have plenty of capacity to lend, Kiefer said.

Interest rate shifts could also lead to more cash-out refis. The prime rate, which climbed to 3.75% in the fourth quarter, could continue to rise if the Federal Reserve proceeds with rate hikes. Credit card debt, largely based on the prime rate, could become more expensive and consumers could use cash-out refis to pay off those cards, Kiefer said.

That’s where the problems could surface for consumers, said the Center for Responsible Lending’s Wolff.

Total household debt rose 2.4% to $12.35 trillion in the third quarter compared to the same period in the previous year, according to the Center for Microeconomic Data at the Federal Reserve Bank of New York. Credit card debt, a portion of that total, rose 4.6% to $747 billion in the same period.

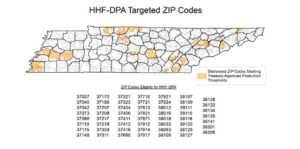

The Tennessee Housing Development Agency is offering $15,000 in down payment assistance to help people who want to purchase a house in certain zip codes.

Couple Ryne Iseminger and Paige Martin recently got engaged and are now talking about purchasing their first home.

“That is definitely something we are discussing. Pretty much daily,” said Iseminger.

After renting a home for nine years, the couple just learned about a new incentive making buying a house in Middle Tennessee an exciting option.

The Tennessee Housing Development Agency received $60 million in federal money from the U.S. Treasury’s Hardest Hit Fund.

Eligible borrowers will have access to that money.

“We will give you $15,000 in down payment and closing costs. It is forgivable over 10 years, no interest during that time, no payments during that time,” explained THDA’s Executive Director Ralph Perrey.

THDA will forgive 20 percent of the loan each year after six years until it is gone if you stay in the house. If the borrower does not refinance, sell, or move out of the home for 10 years, the entire $15,000 loan is forgiven.

“The idea here is to improve those neighborhoods, to strengthen neighborhoods not merely with investment but by the presence of invested home owners,” said Perrey.

Martin told News 2 she is tired of renting.

“You feel like every month when you write a check, it is pretty much going out the door and you will never see it again,” said Martin.

The goal is to revitalize communities in middle Tennessee that never recovered from the economic downturn.

THDA’s $15,000 down payment assistance program is available in 55 targeted zip codes spanning parts of 30 counties across Tennessee.

“That would just be a huge relief and definitely accelerate our plans to be able to move into a neighborhood faster then what we thought,” said resident Nikki Tigg who has been house hunting with her husband.

Fairly or not, the generation of millennials has a reputation as footloose and fancy-free.

Fairly or not, the generation of millennials has a reputation as footloose and fancy-free.

Recent Comments